From News, special focus, page 5 - 8, issue no. 356

compiled by the english edition team

Some love them, some loath them, and others just suspicious of them. They are state-backed giants lighting fires of debate in the global capital markets recently – the sovereign wealth funds (SWFs).

Ailing financial firms on Wall Street have used SWFs like ATM machines while apprehensive congressmen in Washington have called them dangerous players that threaten national security. A January cover of the Economist depicted an invasion of gold bars brought by military choppers dispatched by foreign governments.

Though born in the 1950s, SWFs have renewed interest and debate worldwide last year. As state-funded entities, they rouse suspicion of politically-motivated investments when they acquire strategic businesses and iconic companies in foreign countries. There have been talks of the rise in state capitalism that is encroaching on the free market.

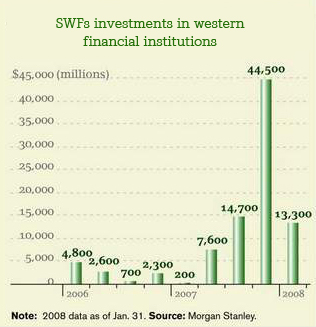

The China Investment Corporation (CIC), one of the youngest SWFs, was under global scrutiny even before its birth last year, and has since fueled a clamor by the US, European Commission and agencies like the International Monetary Fund for regulations and best practices to check on SWFs.

"SWFs are a great way to manage excess government money at this time…They are (governments) planning for the rainy day when they need to take money from the fund," Patrick Flaherty, managing director of

"SWFs are a great way to manage excess government money at this time…They are (governments) planning for the rainy day when they need to take money from the fund," Patrick Flaherty, managing director of

Flaherty, who heads a research team that specializes in SWFs, has said that he expected around 10 to 15 new SWFs to be created in the next ten years, and that three new ones – Japan, Brazil, Saudi Arabia – would be established this year alone. At present, over 20 countries have SWFs.

With SWFs only gaining momentum in global finance, the EO has come up with this special focus on four of the world's top ten SWFs--from

China Investment Corporation (CIC)

China Investment Corporation (CIC)

Background Information: Launched in 2007. Ranks fifth amongst the world's SWF in terms of fund value, which stands at 200 billion dollar at present, or 8% of

Objective: To increase the returns of assets (1.4 trillion dollars worth of foreign exchange reserves); to ease pressure of rising forex reserves; to absorb market liquidity.

Investment Allocation: The Chinese government has announced that CIC's initial investments would be as follow: one third of the capital to buy Central Huijin, which controls

Recent Investments: In December 2007, it invested five billion dollar in Morgan Stanley, the second largest

Related Views and Analysis:

Patrick Flaherty, managing director Amadan International, a

"

Hu Zuliu, Managing Director of Goldman Sachs (

"The rapid economic development of

"CIC should define its operational principles as commercial-based, professional and independent. The SWF charter should clearly state that it is commercially and not politically driven."

Nicolas Véron, fellow researcher of Bruegel, a European think tank devoted to international economics:

"I don't see a fundamental contradiction between the state ownership of assets and the long-term success of the investment strategy, if the governance is appropriate."

"As the Chinese market matures and competition develops, the gains of decentralized decision-making in the corporate world will become clearer. Whether this will lead to large-scale privatization, as has been the case in

Norway's Government Pension Fund- Global (GPF)

Norway's Government Pension Fund- Global (GPF)

Background Information: Launched in 1990. Its fund value has reached over 360 billion dollar, or 93% of

Objective: To use the assets to meet

Investment Allocation: Bonds represent 60% (over half of them AAA-rated) of the portfolio and equities 40%. Its investment in emerging markets is growing. It has an ethical screening process for investment to exclude companies that violate fundamental ethical norms.

Recent Investments: The fund owns shares in about 3,500 companies, mostly holding small stakes below 1%.

Related Views and Analysis:

Geir Vestrum, chief representative of Norges Bank in Shanghai:

"The ministry of Finance designated Norges Bank to manage the fund and decide a benchmark. But they don't interfere with our investment policies. So talking about Norway (GPF), I really don't agree that it is state capitalism.

"What we have encountered are not suspicions, but more of discussion and communication. We believe transparency and openness in investment strategies, goals, performance and risks provide the basis for understanding."

"It was obvious that Wall Street needed money and we just have the capital that they needed. I don't think these investments will create negative impact. Many may say that sovereign wealth funds "rescued" Wall Street. I don't quite agree with the word "rescue". These funds just "helped" Wall Street. Sovereign wealth funds are here to stay in the long run but may not have made headline as they are now. As for whether they will continue to make intense investments, it will depends on capital inflow, investment opportunities and also the market needs."

Government of Singapore Investment Corporation (GIC)

Government of Singapore Investment Corporation (GIC)

Background Information: Launched in 1981. A restructuring in 1999 led to the creation of three operating units: the Public Markets Group to invest in equities, fixed income, and money market instruments; Government of Singapore Investment Corporation (GIC) Real Estate to invest in real estate-related assets; and GIC Special Investments to handle venture capital and private equity funds, as well as direct investments in private companies. Its fund value is between 100 and 330 billion dollar in 2007, 169% of Singapore GDP. It is financed by reserves resulted from high savings rate. It is ranked the world's number three SWF.

Objective: To achieve good returns on state assets; to enhance purchasing power of

Investment Allocation: Diversified Investments in 40 markets.

Recent Investments: January 2008, invested 6.88 billion dollar in the

Related Views and Analysis:

Nicolas Véron, fellow researcher of Bruegel, a European think tank devoted to international economics:

"There has been more apparent willingness to greet SWF money in the

Jennifer Lewis, Head Communications, GIC:

"GIC did not do these investments to bail out the banks or to help stabilize the

"Twenty or thirty years ago when there were just a few of such funds – ourselves, Abu Dhabi, Kuwait – nobody paid much attention to sovereign wealth funds. The term wasn't invented then, and we were able to do our business quietly. But now, many of the funds are being formed - China, Russia, Middle Eastern countries – I think it's understandable that there should be some concern in Europe and America as to what is the agenda of these funds; do they have political motives, are they investing for other than commercial reasons, and our view from Singapore is that these concerns are quite valid and have to be addressed."

"We also felt that if the guidelines (on SWFs) are eventually drawn out, they should be general, flexible, and to some extent voluntary because funds and countries are different… I don't think in this case a one-size-fits-all solution would be possible. The only point which I will make with regard to this request for disclosure and transparency is that I don't think that sovereign wealth funds should be disadvantaged vis-à-vis other investors like fund management companies, like Wellington and Capital, or hedge funds and private equity, which don't have to disclose everything - there should be a level playing field."

Russia

Russia

Background Information: Launched in 2004. Its fund value reached 156.8 billion dollar by January 2008 and has become the sixth largest SWF of the world. Between 2006 and 2007, the fund has had a growth rate of 96%, and is financed by oil-related revenues and taxes on mineral resources. Thanks to skyrocketing global crude oil prices, the fund has expanded quickly and generated returns to pay off 18.3 billion dollar worth of foreign debts prior to the due date. The fund is managed by

Objective: To absorb volatility of commodity prices; to finance the pension fund and to repay foreign debt.

Investment Allocation: Purchases of securities that are issued by governments of US and selected EU countries. Current currency composition: US dollars - 45 %; euros - 45 %; pounds sterling - 10 %.

Related Views and Analysis:

Patrick Flaherty, managing director Amadan International, a

"It must be remembered that for the vast majority of the SWFs, managing oil profits were the reason why these funds were created. These countries are thinking towards the future when their oil runs out. By having this nest egg, they will be able to ride out tough times."

"For most of these states, governments have always taken a very active role in planning the economy. Sovereign Wealth Funds are just another way to plan your economy. They are planning for the rainy day when they need to take money from the fund."

Russian Minister of Finance Aleksey L. Kudrin has said that the fund was established out of concerns over the exhaustion of crude oil in the future, as the Russian economy has been heavily dependent on the export of crude oil and other non-renewable resources.